Fintech is no longer a niche. Payment apps, neobanks, and embedded finance products now touch hundreds of millions of users — including minors. And regulators have noticed.

The COPPA rule amendments that took effect in April 2026, combined with tightening state-level requirements and federal KYC mandates, mean that any fintech product that could reasonably be accessed by someone under 18 (or under 13, depending on the regulation) now needs a defensible age verification strategy. Not a date-of-birth field. Not a checkbox. A real one.

Here’s what’s driving the shift, what the rules actually require, and how to implement age verification in a fintech product without wrecking your onboarding funnel.

Why Fintech Has an Age Verification Problem

Traditional banks solved the minor access problem with physical branches, parental co-signatures, and custodial account structures. Digital-first fintech products blew past those guardrails.

Consider the landscape:

Payment apps like Venmo, Cash App, and Zelle let users send and receive money with minimal friction. Many have no effective age gate beyond a self-declared date of birth at signup. Minors routinely create accounts using fabricated ages — and the platforms know it.

Neobanks targeting teens (Greenlight, Step, Copper) intentionally serve minors, but their age verification and parental consent mechanisms vary wildly in rigor. Some collect a parent’s SSN and run a soft credit check. Others accept a selfie and a name.

Embedded finance — the integration of financial services (payments, lending, accounts) into non-financial apps — creates the most ambiguous scenarios. When a gaming platform, social app, or marketplace embeds a wallet or payment feature, who is responsible for verifying the user’s age? The platform? The banking-as-a-service (BaaS) provider? The sponsor bank?

The regulatory answer is increasingly: everyone in the chain.

The Regulatory Framework: What Fintech Products Must Comply With

Federal KYC Requirements (CIP/CDD)

Under the Bank Secrecy Act and its implementing regulations (31 CFR § 1020.220), every financial institution — including fintechs operating through sponsor banks — must implement a Customer Identification Program (CIP). This requires collecting and verifying:

- Full legal name

- Date of birth

- Address

- Identification number (SSN or equivalent)

For adult customers, this is standard KYC. For minors, it becomes a two-party verification process: you must verify the minor’s identity and the identity and consent of a parent or legal guardian.

The critical point: CIP requirements apply regardless of whether the fintech holds a banking charter. If you’re offering financial products through a BaaS provider or sponsor bank, the compliance obligation flows through to your product. The OCC, FDIC, and CFPB have all issued guidance reinforcing this — fintech partnerships don’t create compliance gaps; they create shared liability.

COPPA and the April 2026 Amendments

The FTC’s updated COPPA rule, with a compliance deadline of April 22, 2026, significantly expands requirements for platforms that collect data from children under 13:

- Broader definition of personal information — Now explicitly includes biometric data, health data, and persistent identifiers used for behavioral advertising

- Stricter consent mechanisms — The FTC has tightened what qualifies as “verifiable parental consent,” moving away from email-plus-delay methods toward more robust verification

- Data minimization — Platforms can only collect data that is “reasonably necessary” for the activity the child is participating in

- Retention limits — Data collected from children must be deleted when it is no longer needed for its original purpose

For fintech products, the February 2026 COPPA policy statement offers a crucial safe harbor: if you collect personal information solely to determine a user’s age, the FTC will not bring an enforcement action — provided you don’t repurpose that data, and you delete it promptly after the age determination is made.

This matters because it resolves the paradox that previously paralyzed compliance teams: “We need to collect data to verify age, but collecting data from minors without consent violates COPPA.” The safe harbor breaks that loop.

State-Level Requirements

The state landscape adds complexity:

Texas (January 2026) — Requires platforms to verify user ages using app store age signals or equivalent methods. Payment apps and neobanks with a mobile presence must integrate Google Play Age Signals or Apple’s Declared Age Range API, or implement their own age verification.

Utah (May 2026) — Mandates age verification at account creation for platforms that could be accessed by minors. Parental consent is required for users under 18. Financial apps are not exempt.

New York — Proposed legislation would require financial apps to implement “commercially reasonable” age verification and restrict certain features (like peer-to-peer transfers above a threshold) for verified minors.

California (AADC) — The Age-Appropriate Design Code requires platforms likely to be accessed by children to conduct Data Protection Impact Assessments (DPIAs) and implement age-appropriate defaults. Fintech apps that serve a general audience fall squarely within scope.

The pattern is clear: states are closing the assumption that financial apps are inherently “adult” products. If a 15-year-old can download your app and create an account, you’re in scope.

EU and UK Requirements

For fintechs operating internationally:

- PSD2 Strong Customer Authentication (SCA) already requires multi-factor identity verification for payment services. Layering age verification into existing SCA flows is architecturally straightforward.

- The EU Digital Identity Wallet (EUDI), rolling out by December 2026, will include age attributes that can be selectively disclosed. Fintechs that accept EUDI wallet credentials will get age verification essentially for free — but only if they’ve built the integration.

- UK Age Assurance standards under Ofcom and the ICO require platforms to use “highly effective” age verification. Self-declaration doesn’t meet the bar.

The Embedded Finance Liability Question

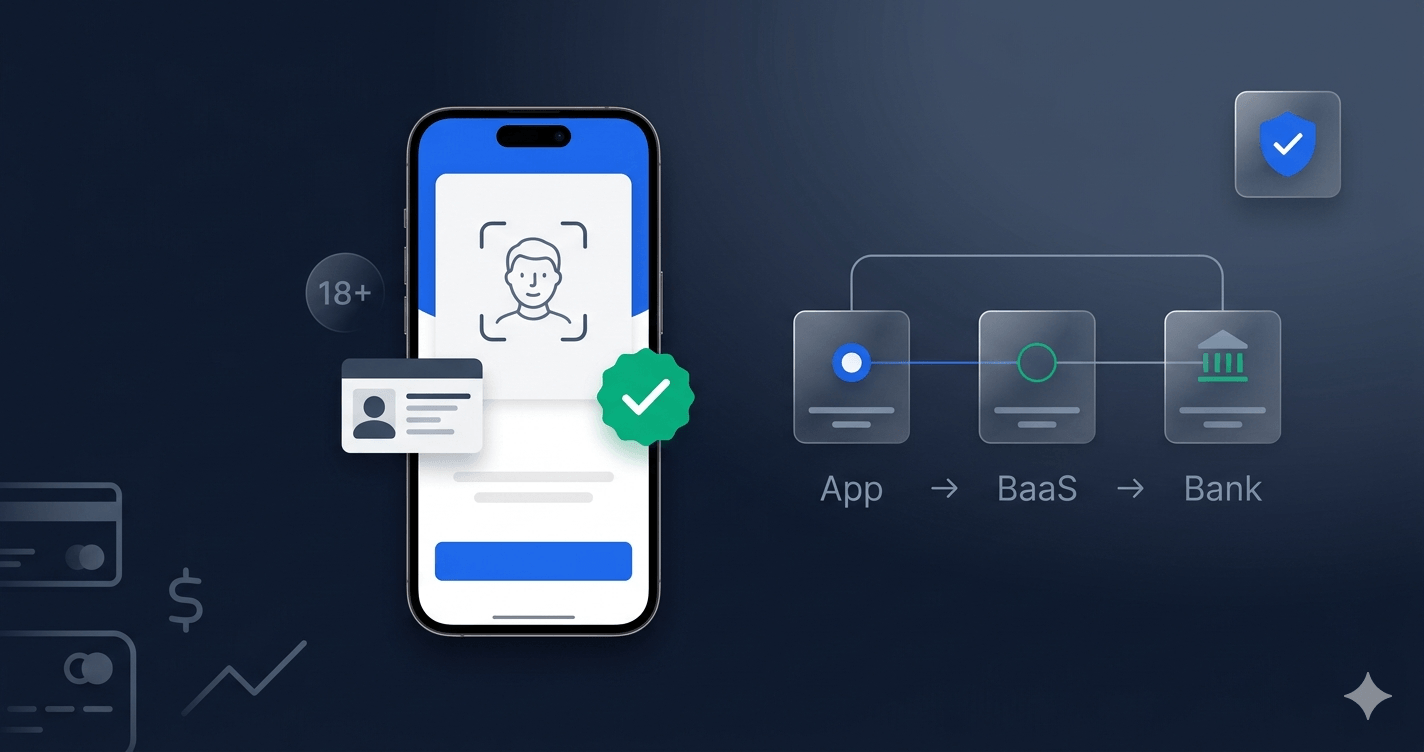

Embedded finance creates a specific and underappreciated liability problem. Consider a typical architecture:

- A consumer app (marketplace, social platform, gaming app) embeds a payment or wallet feature

- The feature is powered by a BaaS provider (Unit, Treasury Prime, Synapse, Bond)

- The BaaS provider operates under a sponsor bank’s charter

When a 14-year-old creates an account on the consumer app and accesses the embedded financial feature, the compliance question is: who was supposed to verify their age?

The regulatory answer, as enforcement actions have made clear, is that all three parties share responsibility:

- The sponsor bank has ultimate regulatory liability under CIP/CDD requirements

- The BaaS provider typically has contractual obligations to implement KYC controls

- The consumer app is the actual point of user interaction — and the entity that chose not to implement age verification at signup

In practice, sponsor banks and BaaS providers are now requiring their fintech partners to implement age verification as a condition of partnership. If you’re building on a BaaS platform in 2026 and you don’t have an age verification strategy, expect your partner to require one — or terminate the relationship.

What Effective Age Verification Looks Like in Fintech

The Two-Tier Model

Fintech products need a two-tier verification approach:

Tier 1: Age determination at signup — Before any account is created, determine whether the user is an adult, a minor (13-17), or a child (under 13). This gates the entire onboarding flow.

Tier 2: Identity verification and consent — For adults, proceed with standard KYC. For minors, trigger the parental consent and custodial account flow. For children under 13, either block account creation or implement full COPPA-compliant consent mechanisms.

Verification Methods That Actually Work

Not all age verification methods are equal. Here’s how they compare for fintech use cases:

Document-based verification (government ID scan + face match) — The gold standard for financial services. You’re already collecting ID for KYC; adding age extraction is trivial. Xident’s document verification extracts date of birth from 6,000+ document types with sub-3-second processing.

AI age estimation (facial analysis) — Useful as a first-pass filter. If the user is clearly over 25 or under 12, you can route them immediately without document friction. For edge cases (13-21), escalate to document verification. Xident’s on-device age estimation runs in the browser via WebAssembly, so no biometric data leaves the user’s device.

NFC chip verification — For users with NFC-enabled identity documents (passports, some national IDs, mobile driver’s licenses), tap-to-verify provides the highest assurance level. The chip contains cryptographically signed data including date of birth. Useful for high-value account creation.

Platform age signals — Google Play Age Signals and Apple’s Declared Age Range API provide age range data for mobile app users. These are useful as supplementary signals but shouldn’t be the sole verification method for financial products.

Reusable age tokens — After initial verification, Xident issues a privacy-preserving age token that lets users prove their age category on subsequent interactions without re-verification. For fintech products with multiple touchpoints (account creation, first transaction, high-value transfers), this eliminates repeated friction.

The Parental Consent Challenge

For fintech products that intentionally serve minors (teen banking apps, family finance tools), parental consent verification is the hardest UX problem. You need to:

- Verify that the minor is actually a minor (not an adult pretending to be one)

- Verify the identity of the parent or guardian

- Verify the relationship between the parent and the minor

- Obtain explicit, informed consent for data collection and account creation

- Provide the parent with ongoing controls and visibility

The temptation is to make this as lightweight as possible. The regulatory requirement is to make it verifiable. These are often in tension.

Xident handles this through a linked verification flow: the minor completes age verification (Tier 1), the system generates a consent request, the parent verifies their own identity and relationship, and consent is recorded with a cryptographic audit trail. The entire flow completes in under 90 seconds.

Implementation: Where to Insert Age Verification

For fintech products, the integration points are:

1. Account Registration

The primary gate. Before creating any account, determine the user’s age category. This is where you decide whether to route to the standard adult flow, the custodial minor flow, or a block.

// Example: Xident SDK integration at registration

const result = await xident.verifyAge({

threshold: 18,

methods: ['estimation', 'document'], // Escalation path

purpose: 'account_creation',

fallback: 'parental_consent' // Route minors to consent flow

});

if (result.ageCategory === 'adult') {

// Proceed to standard KYC

} else if (result.ageCategory === 'minor') {

// Trigger parental consent flow

await xident.requestParentalConsent({

minorToken: result.token,

requiredActions: ['account_creation', 'data_collection']

});

} else if (result.ageCategory === 'child') {

// Under 13: Block or implement full COPPA consent

}2. Feature Gating

Even after account creation, certain features should be gated by age:

- Peer-to-peer transfers above a threshold

- Cryptocurrency trading (restricted to 18+ in most jurisdictions)

- Credit or lending products (legally restricted to adults)

- Investment accounts (custodial requirements apply)

Use Xident’s age token to gate features without re-verification:

const canAccess = await xident.checkAgeToken({

token: user.ageToken,

requiredAge: 18,

feature: 'crypto_trading'

});3. Transaction Monitoring

For products serving both adults and minors, implement age-aware transaction monitoring:

- Flag unusual patterns on minor accounts (large transfers, merchant categories inconsistent with age)

- Notify parents/guardians of transactions above configurable thresholds

- Restrict access to age-inappropriate merchant categories

4. Periodic Re-Verification

Age verification isn’t a one-time event. Users age into new categories. A 17-year-old who created a custodial account should transition to a standard adult account at 18 — but only after re-verification. Implement age milestone triggers:

- At the user’s 13th birthday: transition from child to minor status, expand available features

- At the user’s 18th birthday: prompt for adult verification, remove parental controls if user consents

Conversion Impact: The Numbers

The biggest objection from fintech product teams is always conversion. Here’s what the data shows:

Without age verification: Self-reported date-of-birth fields have a ~12% false age rate among 13-17 year olds (they claim to be 18+). This creates regulatory exposure for every one of those accounts.

With document verification: Expect a 3-7% drop-off at the verification step for adult users. However, Xident’s progressive verification approach (start with AI estimation, escalate only when needed) reduces this to 1-3%.

With reusable tokens: After initial verification, subsequent age checks have zero friction — the token is validated server-side with no user interaction.

Net impact: The small conversion hit at onboarding is offset by reduced fraud, lower chargeback rates on minor-initiated transactions, and elimination of the regulatory risk that comes with unverified minor accounts.

For teen-focused products, age verification actually increases trust. Parents are more likely to approve a product that verifiably checks their child’s age and obtains proper consent.

Building Your Compliance Strategy

Step 1: Map Your Regulatory Surface

Determine which regulations apply to your product:

- Do you operate in states with age verification mandates (TX, UT, CA, NY)?

- Does your product collect data from users under 13 (COPPA)?

- Do you offer financial products through a sponsor bank (CIP/CDD)?

- Do you serve EU/UK users (GDPR, DSA, Age Assurance)?

Step 2: Define Age Categories and Feature Maps

Create a matrix of age categories and the features available to each:

| Feature | Under 13 | 13-17 | 18+ |

|---|---|---|---|

| Account creation | Blocked or COPPA consent | Parental consent | Standard KYC |

| P2P transfers | Blocked | Limited (with parent controls) | Full access |

| Crypto/investing | Blocked | Blocked | Full access |

| Savings/spending | COPPA consent | Parental consent | Full access |

Step 3: Choose Your Verification Stack

Select verification methods appropriate to your risk profile:

- Low-risk features (viewing balance, educational content): Platform age signals or AI estimation

- Medium-risk features (transfers, spending): Document verification or NFC

- High-risk features (lending, crypto): Document verification + liveness detection

Step 4: Implement Progressive Verification

Don’t front-load maximum friction. Use Xident’s escalation model:

- Start with AI age estimation (zero friction for clearly-adult users)

- If age is ambiguous (13-25 range), escalate to document scan

- If document scan indicates minor, trigger parental consent flow

- Issue a reusable age token for all subsequent interactions

Step 5: Audit and Document

Maintain an auditable record of:

- Every age verification attempt (method, result, timestamp)

- Parental consent records (parent identity, consent scope, timestamp)

- Feature access decisions based on age category

- Data deletion compliance for child/minor data

This audit trail is what regulators and sponsor banks will ask for. If you can’t produce it, your compliance program is theater.

What Happens If You Don’t

The consequences of skipping age verification in fintech are escalating:

Regulatory fines — COPPA violations carry penalties of up to $50,120 per violation. With thousands of unverified minor accounts, the math gets painful quickly. The FTC collected over $275 million in COPPA-related penalties between 2019 and 2025.

Sponsor bank termination — BaaS providers and sponsor banks are increasingly conducting compliance audits of their fintech partners. If your product can’t demonstrate adequate age verification, expect remediation demands or partnership termination.

App store removal — Starting in 2026, both Google Play and Apple’s App Store enforce age rating requirements. Apps that don’t implement appropriate age verification may be flagged, restricted, or removed.

Litigation — Class action attorneys have discovered age verification as a growth area. Parents suing fintech products for allowing minors to create unverified accounts is no longer hypothetical.

Reputational damage — A single headline about minors accessing financial products on your platform costs more than any verification implementation.

Getting Started

Xident provides a complete age verification solution for fintech products:

- Multi-method verification: AI age estimation, document verification, NFC chip reading, and platform age signals — all through a single SDK

- Parental consent flows: Built-in consent management with identity verification for both minor and guardian

- Reusable age tokens: Verify once, prove everywhere — eliminate repeated verification friction across features and sessions

- Sub-3-second processing: On-device AI estimation with server-side document verification, keeping latency below the threshold where conversion drops

- 0.03% false pass rate: The lowest in the industry, satisfying even the strictest regulatory standards (Ofcom, KJM, ARCOM)

- Full audit trail: Every verification attempt, consent record, and age-gated decision is logged and exportable for regulatory review

Whether you’re building a teen banking app, embedding payments into a consumer platform, or operating a neobank that serves a general audience, Xident can help you implement compliant age verification without sacrificing the onboarding experience your product depends on.